South Africa Logistics, Warehousing and Cold Chain Market Size and Forecast (2019–2030) - Analysis by Freight Mode (Road, Rail, Marine, Air), Cold Storage, End use Industry and Region

South Africa Logistics and Warehousing Market Size

South Africa’s warehousing market is on a strong growth trajectory, backed by large-scale infrastructure projects like Tambo Springs Logistics Gateway and the Coega SEZ, which are reshaping the country's logistics and distribution landscape.

Modest Growth Amid Rail Recovery and Tariff Pressures

-

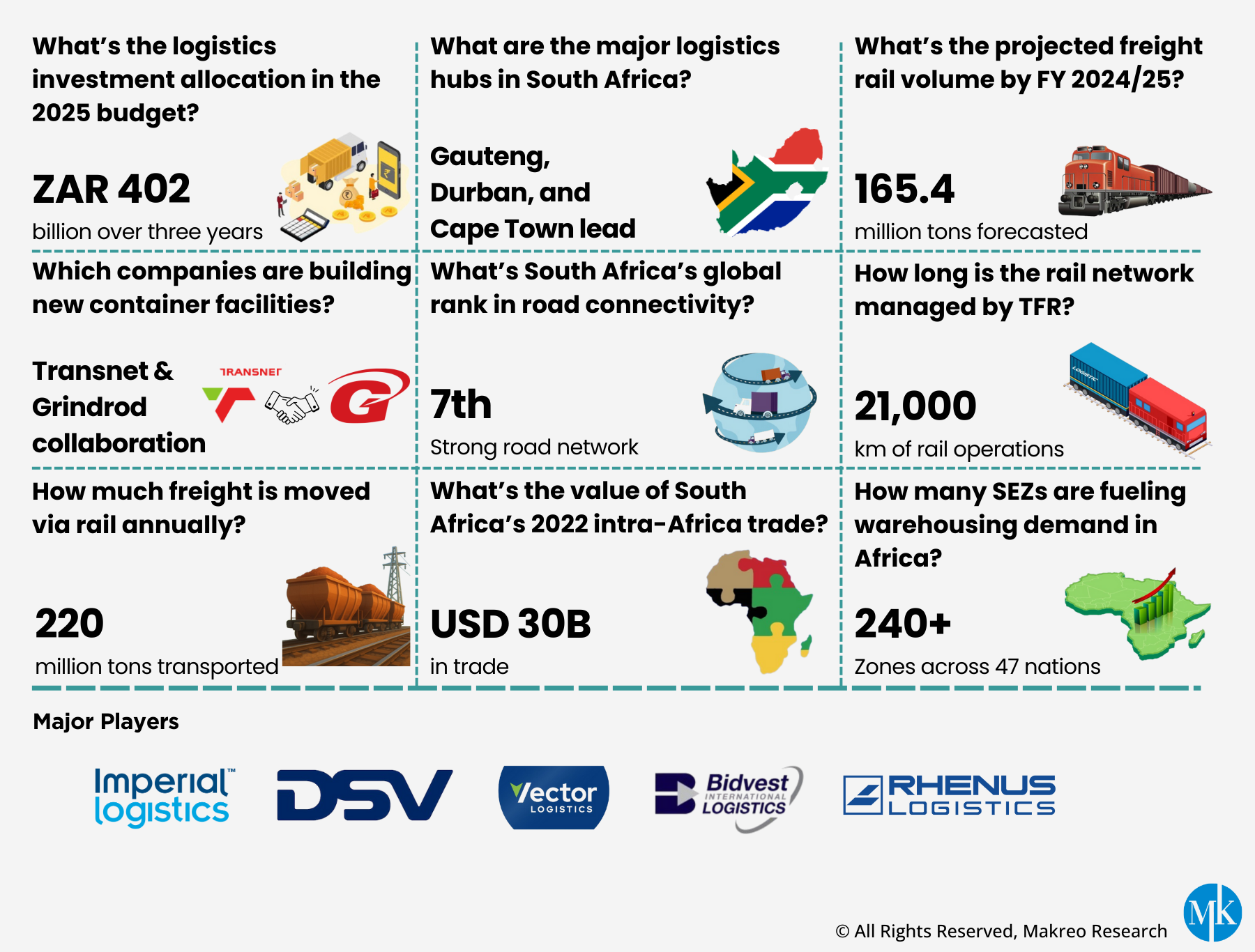

The South African freight and logistics market is projected to exceed USD 30 billion in 2025. This growth is primarily driven by a rebound in rail freight, with Transnet expected to move up to 165 million tons, signaling a positive trend in freight activity. However, growth is moderated by the 30% U.S. tariff on South African exports, which has affected trade volumes and export activities.

-

The South African e-commerce logistics sector is anticipated to expand at a compound annual growth rate (CAGR) of 15.11% between 2025 and 2030. This growth is fueled by increasing digital adoption, better internet penetration, and improvements in logistics infrastructure. The sector is expected to reach a value of USD 17.08 billion by 2030, showcasing robust growth potential across urban and emerging consumer markets.

Scope of the Study for South Africa Logistics Market

Makreo Research presents the report "South Africa Logistics, Warehousing and Cold Chain Market Size and Forecast (2019–2030)," offering a comprehensive overview of the country’s freight transport, warehousing, and cold chain sectors.

The study covers the logistics market across four main freight modes, road, rail, air, and maritime, providing market size data, historical trends, and growth forecasts. It highlights key demand drivers and operational challenges influencing each segment.

In warehousing and cold chain, the report analyzes the distribution and quality of facilities, refrigerated storage capacity, and investment patterns in temperature-controlled logistics. It emphasizes infrastructure gaps in provinces such as Limpopo, Mpumalanga, and Northern Cape, which show potential for expansion.

Rising demand for temperature-sensitive logistics is driven by industries including:

-

Pharmaceuticals, due to growing healthcare logistics and vaccine distribution needs.

-

Food and Beverage, reflecting increased cold storage for perishables.

-

E-commerce, fueling the need for regional fulfillment centers and last-mile cold chain solutions.

The report also profiles leading players based on their storage capabilities, refrigerated fleet size, geographic presence, service offerings, and compliance with standards like ISO and GMP.

South Africa’s Leading Logistics Companies Covered in the Report

The study delivers an in-depth competitive landscape analysis, offering detailed profiles of leading companies operating within South Africa’s logistics, warehousing, and cold chain sectors. Prominent market players such as Imperial Logistics Africa, Vector Logistics (Pty) Ltd., Bidvest International Logistics, DSV South Africa, Rhenus Logistics South Africa (Pty) Ltd., and CCS Logistics Pty Ltd. are thoroughly examined.

Each company profile includes critical operational metrics such as:

-

Warehousing footprint and pallet storage capacity

-

Fleet size and regional service coverage

-

Cold storage and temperature-controlled logistics capabilities

-

Strategic location of facilities and inland logistics hubs

These insights help benchmark company performance and operational strength across the South African logistics and supply chain market.

South Africa Logistics Sector - Strategic Developments and Market Resilience

In addition to operational insights, the report tracks major business developments across the logistics sector, including:

-

Mergers and acquisitions in the South African logistics market

-

Cold chain infrastructure investments

-

Sustainability initiatives and digital transformation in logistics

With a forward-looking perspective and data-backed insights, this report serves as a strategic resource for industry leaders, investors, and policymakers aiming to make informed decisions in an increasingly competitive and evolving South African transportation and logistics environment.

-

Past & Present Analysis: 2019-2024

-

Future Outlook: 2025-2030

-

Base Year: 2024

Freight Transportation Market Segmentation

-

Freight Market Revenue by Mode of Transportation (Road/Rail/Marine/Air)

-

Market Segmentation by Industries

-

Market Segmentation by Shipment Category

-

Market Segmentation by Regions/Cities

Warehousing and Cold Chain Market Segmentation

-

Warehouses Investments

-

by Type of Services

-

by End-User Industry

-

by Geography

Cold Chain Market Segmentation

-

By Type of Cold Storage

-

By Cold Transport

-

Competition

-

Mergers, Acquisitions, and Investments

-

Funding Timeline

-

Company Profiles

South Africa Logistics, Warehousing and Cold Chain Industry Insights

Freight Transport Segment - Backbone of South Africa’s Logistics Market

The freight and logistics market in South Africa is underpinned by robust overland transportation, with road freight emerging as the primary mode of goods movement across the country. Accounting for nearly half of South Africa’s total freight volume, road transport services remain essential to the nation’s logistics and supply chain network, offering critical connectivity between ports, industrial zones, and inland markets.

This segment’s dominance is reinforced by the country's extensive road infrastructure, which supports both short-haul and long-distance freight transportation. Despite ongoing investments in rail logistics, the flexibility and faster turnaround of road-based logistics solutions continue to make road freight the backbone of South Africa’s transportation and logistics sector.

South Africa Freight Market by Shipment Category (%), 2024

Expansion and Modernization in the Warehousing and Cold Chain Segment

In January 2024, Rhenus South Africa further strengthened its position along the East Coast by opening a 3,000 m² warehouse in Samrand near Pretoria, along with a 2,000 m² facility in East London. This expansion reflects the growing demand for efficient warehousing services in South Africa. The trend continued in February 2024, as M24 Logistics launched a 30,000 m² state-of-the-art warehouse in Montague Gardens, aimed at serving both B2B and e-commerce clients.

Cross-Border Infrastructure Projects Strengthen Intra-African Trade Logistics

In March 2024, South Africa and Namibia unveiled infrastructure development projects valued at USD 411.9 million over the next three years. These initiatives focus on improving the rail and port infrastructure to address current inefficiencies within the logistics sector. As part of the commitment, Namibia’s Ministry of Finance has allocated USD 117.69 million in 2024 to enhance cross-border connectivity between the two nations and other key regions of Southern Africa.

South Africa Warehousing and Cold Chain Market, 2019 - 2024

South Africa Cold Chain Logistics - Boosting Export Growth and Infrastructure Demand

The cold chain logistics sector is pivotal in ensuring the safe transportation of perishable agricultural and pharmaceutical products, maintaining their quality from origin to destination. With the increasing demand for efficient and reliable cold chain services, the need for advanced infrastructure has surged. This is particularly driven by the growing focus on export growth, as businesses aim to preserve product integrity throughout the supply chain. As a result, there is a heightened focus on expanding and upgrading South Africa's cold chain logistics infrastructure to support the evolving demands of global trade and local markets.

Bidvest Group Limited (Global) Freight Segment Revenue, FY’2019 – FY’2024

Bidvest Group’s Freight Division Reports Resilient Growth

The Freight Division of Bidvest Group Limited has shown impressive growth despite a high performance base from the previous year. Revenue increased by over 4%, reaching ZAR 8.8 billion. This growth was fueled by annual price adjustments, a rise in oil and gas activities in Namibia, successful new business acquisitions, and an improved product mix within terminal operations.

DHL Africa Business Highlights

DHL Supply Chain has partnered with Scania to enhance road transport efficiency in Kenya. In March 2025, DHL and Scania introduced 25 new Euro 5 biodiesel-powered trucks in Kenya, marking the first deployment of such vehicles in both Kenya and the wider East African region. This partnership underscores their commitment to advanced, fuel-efficient technology, improving road safety, and enhancing fuel efficiency through driver training and telematics.

Companies Covered in the South Africa Logistics and Warehousing Market

-

Imperial Logistics Africa

-

Vector Logistics (Pty) Ltd.

-

Bidvest International Logistics

-

DSV South Africa

-

Rhenus Logistics South Africa (Pty) Ltd

There are 16 players covered in this report. To know more, please reach out to sales@makreo.com