Egypt Logistics, Warehousing and Cold Chain Market Size and Forecast (2021–2030) - Analysis by Warehouse Type (Dry, Cold Storage, Bonded and Distribution Center), Freight Type, Cold Chain Capacity, 3PL Services, End-Use Industry and Geography

Egypt Logistics, Warehousing and Cold Chain Market Growth

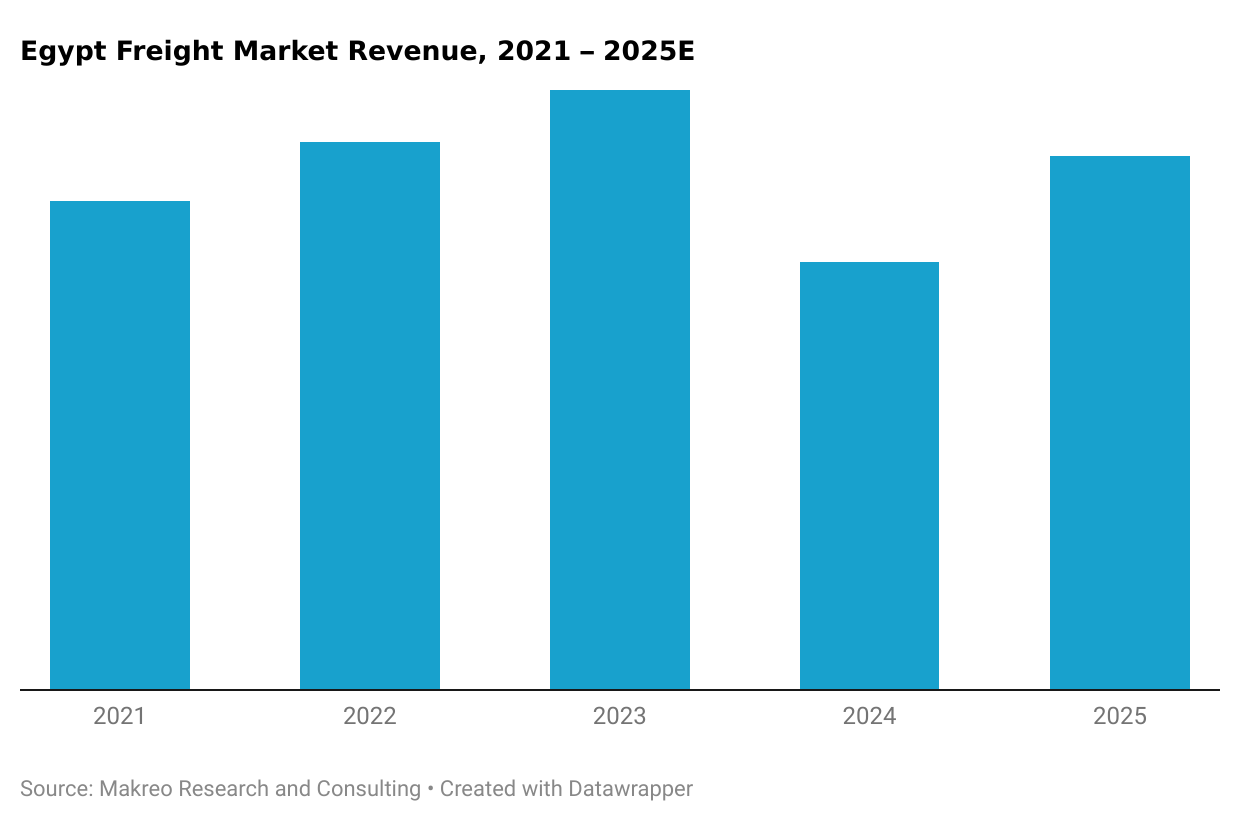

Egypt’s logistics, warehousing, and cold chain market is experiencing sustained growth, supported by the country’s strategic geographic location, rising international and domestic trade flows, and improving cost competitiveness. Between 2021 and 2025E, the Egypt logistics market expanded by more than USD 3 billion in revenue, reflecting higher port throughput, strengthening domestic distribution demand, and gradual modernization across logistics and warehousing infrastructure. Handling an estimated 1.5% to 1.7% of global seaborne cargo, Egypt has reinforced its role as a key maritime and logistics gateway connecting Europe, Asia, and Africa.

This growth trajectory is further supported by Egypt’s favorable operating economics within the MENA logistics landscape. In 2023, the country ranked third in maritime connectivity after the UAE and Saudi Arabia, indicating solid integration with global shipping routes. At the same time, extremely competitive industrial wage levels, around USD 138 per month versus almost USD 2,000 in Saudi Arabia, combined with lower overall operating costs and the depreciation of the Egyptian pound, have strengthened Egypt’s appeal as a regional hub for logistics, warehousing, and cold chain operations. These structural advantages are expected to underpin market expansion and investment momentum over the forecast period.

Freight Demand Structure Driving Growth in the Egypt Logistics Market

-

Freight demand in Egypt remains highly concentrated across a limited number of core sectors, with agriculture, manufacturing, construction, wholesale & retail trade, and oil & gas accounting for the majority of total freight transport volumes in 2024. This concentration continues to directly support expansion across the Egypt logistics, warehousing, and cold chain market.

-

The manufacturing sector, contributing approximately 17% of Egypt’s GDP, generates strong inbound flows of raw materials and outbound movement of finished goods, sustaining demand for dry warehousing, distribution, and value-added logistics services.

-

The construction sector remains one of the fastest-growing freight-intensive industries, supported by large-scale infrastructure development and government-led megaprojects, driving high volumes of bulk transport and storage demand.

Looking for a Section from Report? Start your Partial Purchase Request

Egypt Logistics, Warehousing and Cold Chain Industry Insights

Egypt Maritime Infrastructure and Suez Canal Disruption Impact

-

In 2023, Suez Canal experienced a sharp contraction in activity across all vessel categories. Total transits declined by approximately 50% year-on-year, while cargo volumes fell by over 60% and net tonnage dropped by 66%. These declines reflect the impact of global trade disruptions and large-scale rerouting of maritime traffic amid heightened geopolitical tensions.

-

Despite this short-term disruption, Egypt retains a highly strategic maritime position at the intersection of Africa, Asia, and Europe, with direct access to both the Mediterranean Sea and the Red Sea, reinforcing its long-term importance within global shipping and trade networks.

-

Egypt manages more than 2,000 km of coastline and operates approximately 15 commercial seaports, comprising six Mediterranean ports (Alexandria, Damietta, Port Said, Dekheila, El-Arish, and Abu Qir) and nine Red Sea ports (Sokhna, Adabiya, Safaga, Nuweiba, Suez, Sharm El-Sheikh, Hurghada, Al-Tor, and Berenice), providing extensive coverage across key international and regional maritime routes.

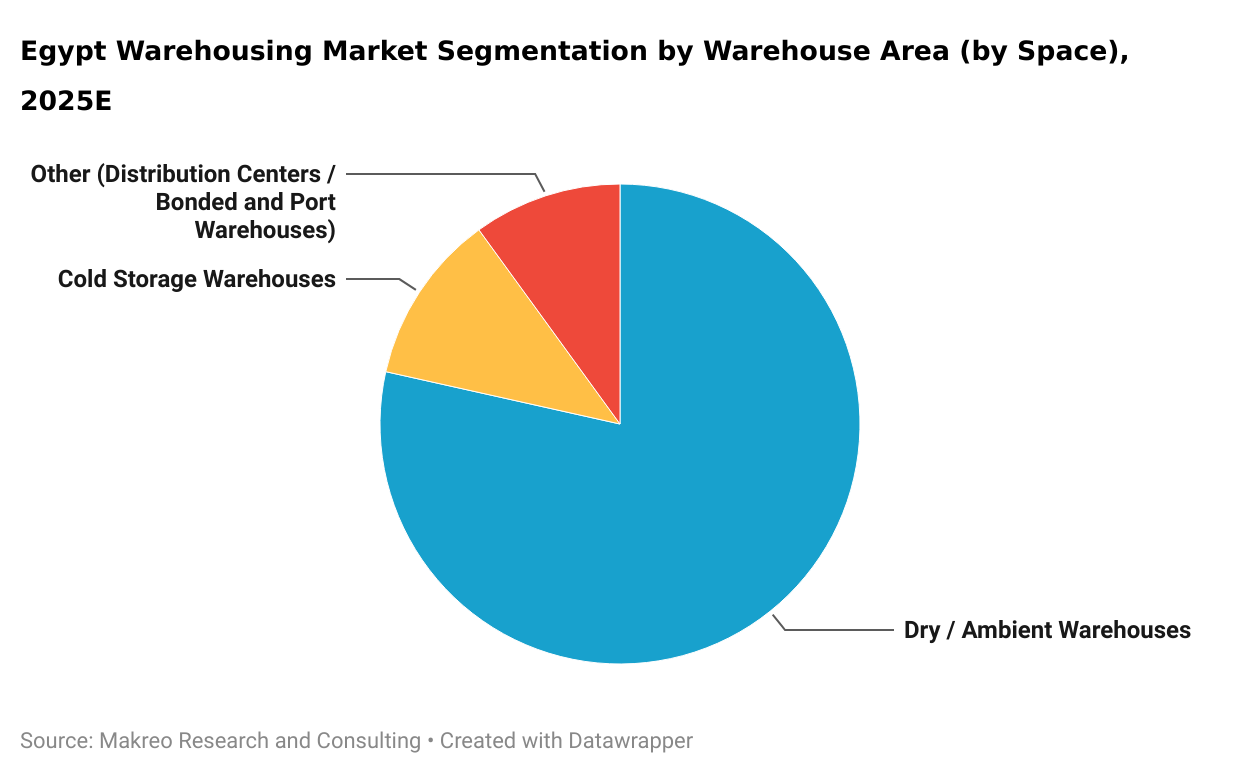

Demand-Led Structure of the Egypt Warehousing Market by Facility Type

-

Dry and ambient warehouses continue to form the backbone of the Egypt warehousing market, supported by sustained demand from FMCG, retail, textiles, and industrial manufacturing sectors. These users prioritize cost-efficient, non-temperature-controlled storage to support high-volume distribution and inventory turnover.

-

Cold storage remains a smaller but steadily growing segment, with demand led by food processing, agribusiness, pharmaceuticals, and export-oriented supply chains. Key users include Lactalis Egypt, pharmaceutical distributors, and fresh produce exporters supported by Multi Fruit Egypt, reflecting rising requirements for temperature-controlled logistics.

-

Distribution centers, bonded warehouses, and port-adjacent facilities are gaining importance amid growth in e-commerce and trade activity. Demand is driven by platforms such as Jumia and Amazon, alongside import-export operations and customs-linked logistics needs.

-

On the supply side, operators including LATT Logistics and Globelink Egypt are expanding strategically located bonded warehouses and container freight stations (CFS) to support port-based storage and international trade flows.

-

Overall, Egypt’s warehousing market remains demand-led, anchored by ambient storage. Capacity additions in cold chain and bonded facilities are selective and aligned with higher-value, regulated, and trade-driven logistics demand.

Scope of the Study for Egypt Logistics, Warehousing and Cold Chain Market

Makreo Research presents the report titled "Egypt Logistics, Warehousing and Cold Chain Market Size and Forecast (2021–2030) - Analysis by Warehouse Type (Dry, Cold Storage, Bonded and Distribution Center), Freight Type, Cold Chain Capacity, 3PL Services, End-Use Industry and Geography" The study delivers a comprehensive evaluation of the Egypt logistics market, encompassing freight transportation, warehousing, third-party logistics (3PL), and temperature-controlled supply chain services. The study evaluates market size, growth trends, infrastructure development, and competitive dynamics, positioning Egypt as a strategic logistics hub connecting Africa, the Middle East, and Europe.

Egypt Logistics, Warehousing, and Cold Chain Market Coverage

-

Comprehensive market coverage of logistics, warehousing, and cold chain services across Egypt, spanning freight transport, storage, distribution, and temperature-controlled operations.

-

Assessment of market transformation drivers, including:

-

Rising industrial and manufacturing activity

-

Expansion of logistics parks, ports, and industrial infrastructure

-

Shifts in regional and international trade flows

-

-

Evaluation of Egypt’s evolving role as a regional and intercontinental logistics gateway

Egypt Logistics Infrastructure Development Assessment

-

Review of major logistics infrastructure developments, including:

-

Suez Canal Economic Zone (SCZone) industrial and logistics clusters

-

Port modernization and capacity expansion projects

-

Development of multimodal connectivity across road, rail, sea, and air networks

-

Policy and Regulatory Environment in the Egypt Logistics Market

-

Assessment of government reforms and policy initiatives shaping the evolution of the Egypt logistics, warehousing, and cold chain market.

-

Modernization of the logistics sector

-

Expansion of warehousing and temperature-controlled capacity

-

Increased private sector participation and foreign direct investment (FDI) in logistics infrastructure.

-

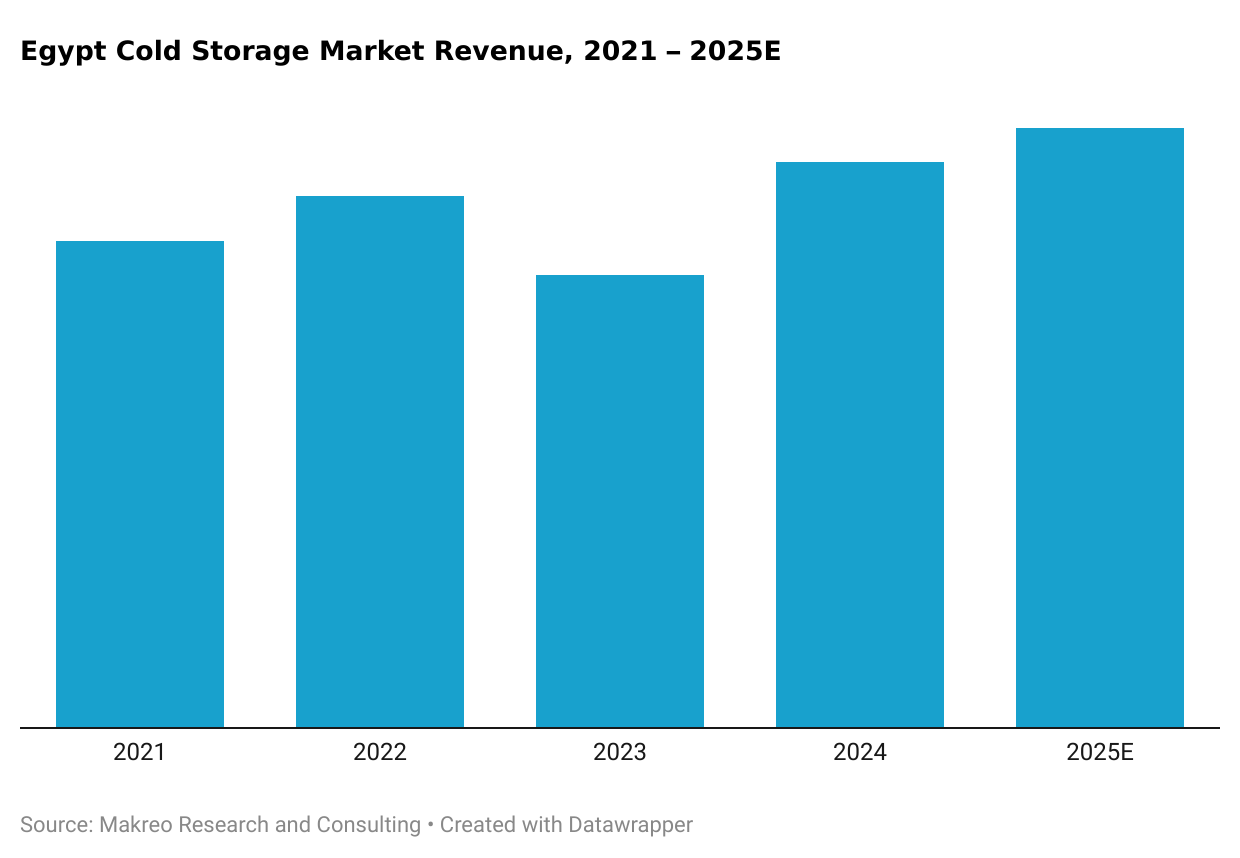

Egypt Cold Chain Logistics Market Growth and Capacity Expansion

-

The Egypt cold chain logistics market recorded steady expansion between 2021 and 2025, adding approximately USD 100 million in market value, supported by rising demand for temperature-controlled storage and transportation. Growth momentum is expected to continue over 2025–2030, with the market projected to expand at a high single-digit CAGR, driven by increasing perishable food exports, growing pharmaceutical distribution requirements, and rising consumer preference for fresh and processed food products.

-

Alexandria remains a core hub for cold chain activity due to its role as Egypt’s primary port city, handling over 60% of the country’s international trade. According to the Alexandria Port Authority, the port offers extensive storage infrastructure, including specialized refrigerated facilities designed to handle large volumes of temperature-sensitive cargo, supporting both imports and export-oriented cold chain flows.

-

On the supply side, new large-scale cold storage developments are underway to address capacity gaps. Notable projects include a 25,000-pallet cold storage facility in the Al Oula region, developed in partnership with DP World, aimed at strengthening refrigeration infrastructure for fruits, vegetables, dairy products, and other perishable commodities, and improving Egypt’s cold chain readiness for domestic distribution and exports.

Egypt Logistics Market Outlook and Growth Forecast

Looking ahead, the Egypt logistics market is expected to record robust expansion between 2025E and 2030F, with industry revenues projected to increase by more than USD 10 billion, supported by rising trade activity and continued infrastructure investment. Over this period, Egypt is set to significantly enhance its agricultural export capacity while simultaneously strengthening domestic food-security infrastructure. Record export volumes, combined with ongoing investments in cold chain, warehousing, and agro-processing facilities, are expected to create a favorable operating environment and position the logistics sector as an increasingly attractive opportunity for private investors over the medium term.

-

2021–2025: Past and Present Performance

-

2025: Base year

-

2026–2030: Outlook

Egypt Logistics, Warehousing and Cold Chain Market Segmentation

-

Freight Transport

-

Warehousing

-

Value-Added Services / 3PL

-

Road Freight

-

Rail Freight

-

Marine Freight (Sea Cargo)

-

Air Freight

-

Domestic Freight

-

International Freight

-

Containerized Cargo

-

Bulk Cargo (Dry & Liquid)

-

Break Bulk

-

Perishables

-

Express & High-Value Goods

-

Public Sector Entities (Port Authorities, Egyptian National Railways)

-

Private Logistics Operators

-

Freight Forwarders

-

Public–Private Partnership (PPP) Projects

-

Dry / Ambient Warehouses

-

Cold Storage Warehouses

-

Distribution Centers / Bonded & Port Warehouses

-

Large Warehouses

-

Medium Warehouses

-

Small Warehouses

-

Cold Storage Revenue

-

Cold Transport Revenue

-

Chilled (0–10°C)

-

Frozen (below −18°C)

-

Deep Frozen (below −25°C)

Geography Assessed

-

Greater Cairo

-

Alexandria

-

Suez Canal / Port Cities

-

Upper Egypt / Delta

-

Mediterranean Corridor (Alexandria–Cairo)

-

Port Said Cluster (East & West Port Said / Transshipment)

-

Damietta Port Corridor

-

Red Sea Corridor (Ain Sokhna–Suez–Safaga)

-

Suez Canal Economic Zone (SC Zone)

-

Greater Cairo (including 6th of October City)

-

Alexandria

-

Suez Canal / Port Region

-

Other Regions

-

Greater Cairo

-

Alexandria

-

Suez Canal / Port Cities

-

Upper Egypt / Delta

Companies Covered in the Egypt Logistics and Warehousing Market

-

Egyptian Global Logistics S.A.E

-

Logistica For Logistic Services S.A.E

-

LATT Logistics

-

Transmar International Shipping Company

-

Transcargo International S.A.E. (TCI)

-

Multi Fruit Egypt

There are 18 players covered in this report. To know more, please reach out to sales@makreo.com

Table of Contents

- 1.Research Methodology

- 1.1.Objective of the Study

- 1.2.Market Definitions and Key Terminologies

- 1.3.Research Design and Procedure

- 1.4.Research Methodology

- 1.5.Data Collection Methods

- 2.Egypt Trade and Logistics Competitiveness Overview

- 2.1.Egypt and MENA Freight Infrastructure Quality and Operating Cost

- 2.2.Egypt and MENA Maritime Partners and Air Links Comparison

- 2.3.Major Bilateral Trade and Investment Agreements of Egypt

- 3.Egypt Logistics Market Past and Present Performance

- 3.1.Egypt Logistics, Warehousing and Cold Chain Market Past and Present Performance

- 3.2.Egypt Logistics Market Past and Present Performance

- 3.3.Egypt Major Logistics, Industrial, and Cold-Chain Infrastructure Investments

- 3.4.Egypt Logistics Market Segmentation Overview

- 3.4.1.Segmentation by Service Type, End User and Geography

- 4.Egypt Freight Market Past and Present Performance and Modal Analysis

- 4.1.Egypt Freight Market - An Overview

- 4.2.Egypt Freight Market Past and Present Performance

- 4.2.1.Egypt Freight Market by Modes (Rail, Road, Air and Marine) - Past and Present Performance

- 4.3.Egypt Freight Transportation Domestic and International Mode of Transport

- 4.4.Egypt Freight Share by Geography / Trade Corridor

- 4.5.Egypt Freight Transport and Port Performance Analysis

- 4.6.Egypt Freight Market by Key Industry Sectors

- 4.7.Egypt Freight Market - Demand and Supply Insights

- 5.Analysis of Suez Canal Performance and Strategic Outlook

- 6.Egypt Maritime Cargo and Port Operations Overview

- 6.1.Egypt Marine Cargo Overview

- 6.2.Egypt Traffic at Different Seaports

- 7.Egypt Road Freight Analysis

- 7.1.Egypt Road Freight Overview

- 7.1.1.Egypt Road Freight Fleet Overview

- 7.1.2.Egypt Road Freight Volume and Revenue

- 7.1.Egypt Road Freight Overview

- 8.Egypt Air Cargo Analysis

- 8.1.Egypt Air Cargo Overview

- 8.2.Egypt Air Cargo Revenue

- 9.Egypt Rail Freight Analysis

- 9.1.Egypt Rail Freight Overview

- 9.1.1.Egypt Rail Freight Volume and Revenue

- 9.1.Egypt Rail Freight Overview

- 10.Egypt Warehousing Market Past and Present Performance

- 10.1.Egypt Warehousing Market – An Overview

- 10.2.Egypt Warehousing Market Past and Present Performance

- 10.3.Egypt Warehousing Market - Demand and Supply Analysis

- 10.4.Egypt Warehousing Market Segmentation Overview

- 10.4.1.Egypt Warehousing Market Segmentation by Warehouse Type

- 10.4.2.Egypt Warehousing Market Segmentation by Warehouse Area

- 10.4.3.Egypt Warehousing Market Segmentation by Regions

- 11.Egypt Warehousing Rental Rates

- 11.1.African Countries Warehousing Rental Rates Comparison

- 11.2.Egypt Warehousing Rental Rates

- 11.3.Cairo Warehousing Rental Rates

- 11.4.Alexandria Warehousing Rental Rates

- 12.Cairo Warehouse Area and Rental Rates Analysis by Different Districts

- 13.Egypt Types of Warehouses by State/Territory

- 14.Egypt Warehouse Silos Analysis

- 15.Egypt Cold Chain Market Past and Present Performance

- 15.1.Egypt Cold Chain Market – An Overview

- 15.2.Egypt Cold Chain Market Past and Present Performance

- 16.Egypt Cold Chain Market Segmentation

- 16.1.Egypt Cold Chain Market Segmentation Overview

- 16.1.1.Egypt Cold Chain Market Segmentation by Function

- 16.1.2.Egypt Cold Chain Market Segmentation by Temperature Range

- 16.1.3.Egypt Cold Chain Market Segmentation by End-Use Industry

- 16.1.4.Egypt Cold Chain Market Segmentation by Geography

- 16.1.Egypt Cold Chain Market Segmentation Overview

- 17.Egypt Cold Chain Facilities and Capacities

- 18.Egypt Third Party Logistics (3PL) Market Past and Present Performance

- 18.1.Egypt 3PL Market Past and Present Performance

- 18.2.Egypt 3PL Market Segmentation Overview

- 18.2.1.Egypt 3PL Market Segmentation by Service Type

- 18.2.2.Egypt 3PL Market Segmentation by End User

- 19.Major Industrial Zones within the Suez Canal Economic Zone (SCZONE)

- 19.1.Egypt Industrial Zones Overview

- 19.2.Key Industrial Zones under Suez Canal Economic Zone (SCZONE)

- 20.Egypt Major Ports Infrastructure, Expansion & Performance

- 20.1.Major Egyptian Ports - Infrastructure & Development Overview

- 20.2.Port Activity and Throughput Metrics for SC Zone Ports

- 20.3.Alexandria Port Authority Expansion Initiatives

- 20.4.Red Sea Port Infrastructure Expansion

- 20.5.Damietta Port Development Initiatives

- 20.6.Port Said Tonnage Throughput and Cargo Performance

- 20.7.El Dekheila and Al Adabiya Port Tonnage Throughput and Growth Rate

- 20.8.Sokhna Port Tonnage Throughput and Growth Rate

- 21.Egypt Key Industry Analysis

- 21.1.Egypt Key Industry Market Overview

- 21.2.Egypt Food & Retail Industry Landscape

- 21.3.Egypt Pharmaceutical Manufacturing Capacity and Future Investment Outlook

- 21.4.Egypt Automotive Manufacturing Capacity and OEM Partnerships

- 21.5.Egypt E-commerce Landscape and Online Trends

- 22.Egypt Trade Performance

- 22.1.Egypt Trade Performance Overview

- 22.2.Egypt Export of Goods Trends

- 22.3.Egypt Import of Goods Trends

- 23.Egypt Freight Market Competitive Landscape

- 23.1.Egypt Freight Market Key Players Performance Scorecard

- 23.2.Egypt Freight Market Key Players by Mode of Coverage

- 23.3.Egypt Freight Market Key Players by Innovation

- 23.4.Egypt Freight Market Key Players Turn-around Times (TT)

- 23.5.Egypt Freight Market Top Digital Freight Platforms and Compliance Certifications

- 23.6.Egypt Freight Market Key Players by Network Coverage (Industrial Zones and Ports)

- 23.7.Egypt Freight Market Key Startup Players

- 24.Egypt Warehousing Market Competitive Landscape

- 24.1.Egypt Top Players by Warehousing Space

- 24.2.Egypt Warehousing Market Area and Capacity

- 24.3.Egypt Warehousing Market Warehouse Footprint & Logistics Park Space

- 24.4.Egypt Warehousing Market Certifications and Compliances

- 25.Egypt Cold Chain Market Competitive Landscape

- 25.1.Egypt Cold Storage Key Players Capacity Comparison

- 25.2.Egypt Cold Storage Market Key Players by Temperature Ranges

- 25.3.Egypt Top Companies Fleet Size and Key Metrics Comparison

- 26.Mergers /Acquisitions/ Investments/ Disinvestments

- 26.1.Mergers /Acquisitions/ Investments/ Disinvestments

- 27.Funding Timeline

- 27.1.Funding Timeline

- 28.Egypt Integrated Logistics / 3PL Company Profiles

- 28.1.Player 1 - Business Overview

- 28.1.1.Business Highlights

- 28.2.Player 2 - Business Overview

- 28.3.Player 3 - Business Overview

- 28.4.Player 4 - Business Overview

- 28.5.Player 5 - Business Overview

- 28.5.1.Business Highlights

- 28.5.2.Business Financials

- 28.5.3.Operational Case Studies

- 28.1.Player 1 - Business Overview

- 29.Egypt Freight Transport & Shipping Company Profiles

- 29.1.Player 1 - Business Overview

- 29.1.1.Timeline

- 29.1.2.Business Highlights

- 29.2.Player 2 - Business Overview

- 29.3.Player 3 - Business Overview

- 29.3.1.Business Highlights

- 29.3.2.Business Financials

- 29.4.Player 4 - Business Overview

- 29.4.1.Business Highlights

- 29.4.2.Business Financials

- 29.5.Player 5 - Business Overview

- 29.5.1.Business Highlights

- 29.5.2.Business Financials

- 29.6.Player 6 - Business Overview

- 29.6.1.Business Overview and Highlights

- 29.6.2.Key Highlights

- 29.7.Player 7 - Business Overview

- 29.1.Player 1 - Business Overview

- 30.Egypt Warehousing Company Profiles

- 30.1.Player 1 - Business Overview

- 30.2.Player 2 - Business Overview

- 30.3.Player 3 - Business Overview

- 31.Egypt Cold Chain Logistics Company Profiles

- 31.1.Player 1 - Business Overview

- 31.2.Player 2 - Business Overview

- 31.3.Player 3 - Business Overview

- 31.3.1.Business Highlights

- 32.Egypt Logistics, Warehousing and Cold Chain Market Challenges

- 33.Egypt Logistics, Warehousing and Cold Chain Market Opportunities

- 34.Egypt Logistics, Warehousing and Cold Chain Market Future Outlook

- 34.1.Egypt Logistics, Warehousing and Cold Chain Market Outlook

- 34.2.Egypt Logistics Market Outlook

- 34.3.Egypt Freight Market Outlook

- 34.4.Egypt Warehousing Market Outlook

- 34.5.Egypt Cold Chain Market Outlook

- 34.6.Egypt 3PL Market Outlook

- Limitations of the Study

Related Reports — Automotive & Transportation