Egypt Warehousing and Cold Chain Market Size and Forecast (2021–2030) - Analysis by Warehouse Type, Temperature Range (Chilled, Frozen, Deep-Frozen), Cold Storage Capacity, End-Use Industry and Geography

Egypt Warehousing Market Size

In 2025, the Egypt warehousing market was valued at over USD 4 billion, supported by ongoing industrial expansion, resilient retail activity, and rising demand for modern storage infrastructure. The market is expected to record steady growth, reaching approximately USD 7 billion by 2030, reflecting a CAGR of 9.20% over the forecast period.

Amid ongoing regional security challenges, major global shipping lines were compelled to reroute vessels around the Cape of Good Hope as an alternative to the Red Sea passage. This diversion significantly reduced vessel movement through the Bab al-Mandab Strait and the Suez Canal - two of the world’s most critical maritime trade corridors. As a result, transit times increased by almost 2 weeks, raising freight costs and disrupting supply chains. Between late 2023 and early 2024, these disruptions contributed to ~60% decline in average daily transit trading volumes, highlighting the deep impact on Egypt’s logistics and port activity.

Abu Rawash Warehousing and Logistics Hub - Strategic Location Advantage

Abu Rawash is located on the northwestern periphery of Greater Cairo, strategically positioned between two critical transport corridors: the Rod El Farag Axis and the Cairo–Alexandria Desert Road. The latter serves as the primary arterial route linking Cairo with Alexandria, Egypt’s principal seaport. Its strategic placement makes it an ideal hub for receiving cargo from Alexandria and efficiently distributing goods across Cairo.

Advantages

-

Nearest warehousing cluster to the new Sphinx Airport

-

Strong connectivity to key transportation routes and logistics nodes

Challenges:

-

Limited availability of land and a shortage of modern Grade A warehousing facilities

Looking for a Section from Report? Start your Partial Purchase Request

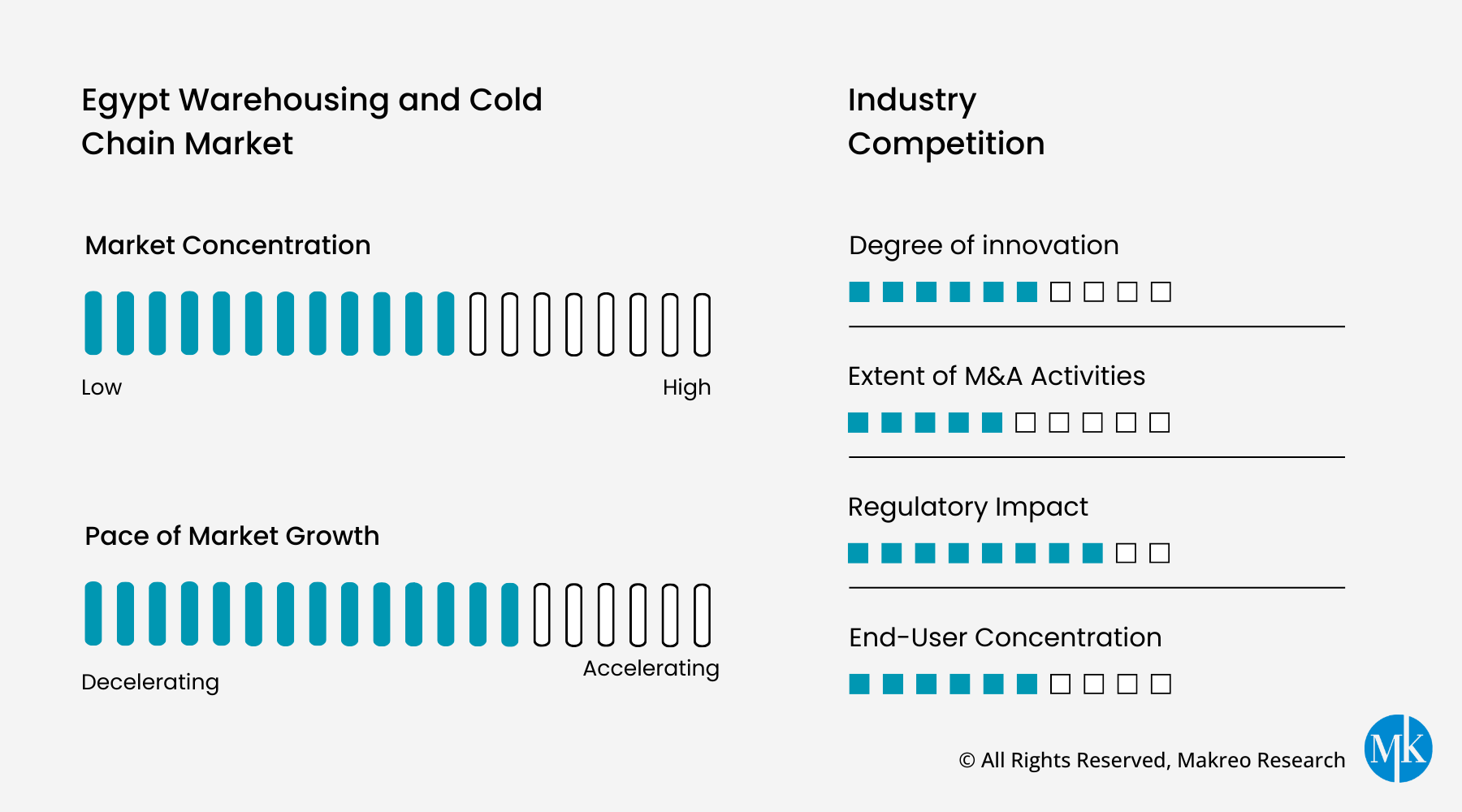

Egypt Warehousing and Cold Chain Industry Insights

Egypt Grade A Warehousing Market Dynamics and Supply Constraints

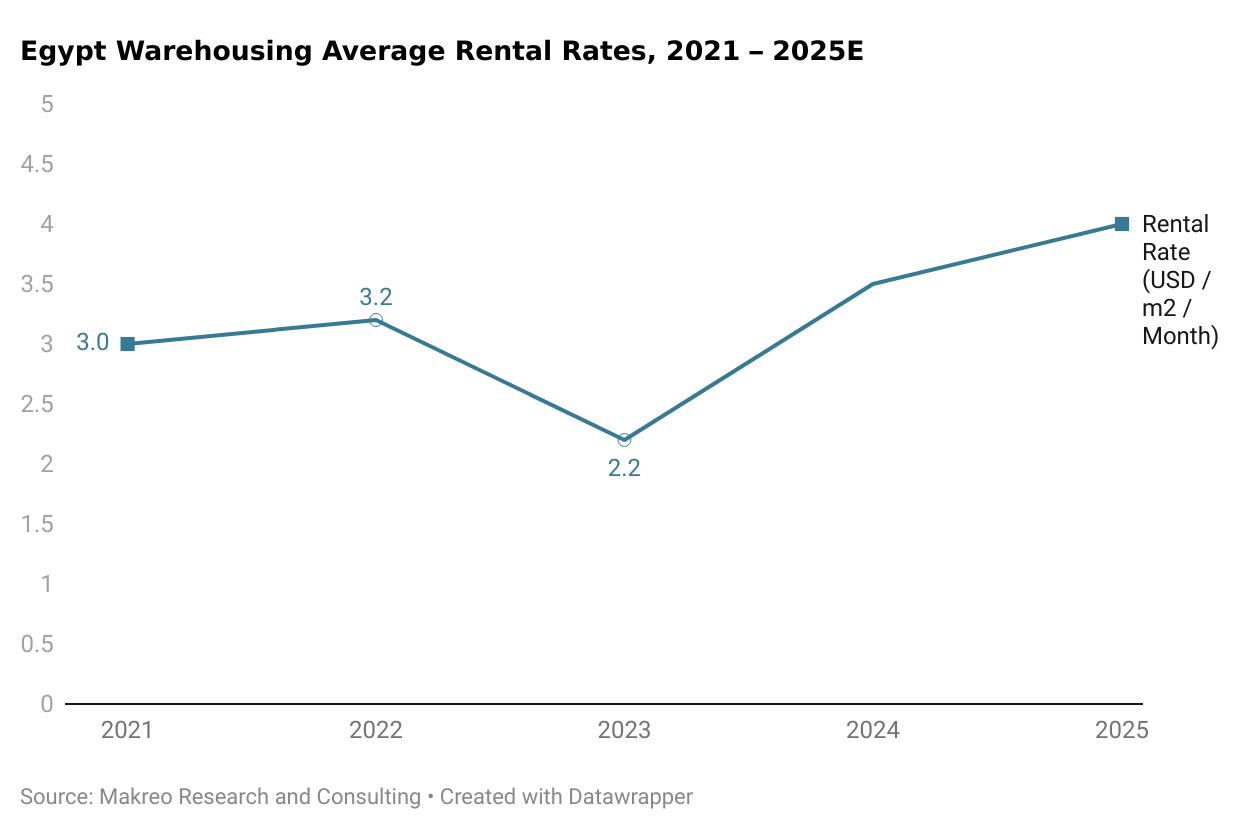

The sharp depreciation of the Egyptian pound has catalyzed increased investment activity across the real estate sector, particularly in commercial and industrial assets, as investors increasingly view property as a hedge against currency volatility. Despite broader market uncertainty, prime warehousing rents remained largely stable during the first nine months of 2024, reflecting sustained demand for quality logistics and storage facilities.

However, the availability of Grade A industrial warehousing in Egypt remains structurally constrained. Supply has not expanded at a pace sufficient to meet the requirements of manufacturers, distributors, and retailers seeking modern, compliant, and strategically located facilities. As major infrastructure initiatives, including logistics parks, transport corridors, and industrial zones, progress toward completion, demand for high-quality warehouse stock is expected to strengthen further. This imbalance is likely to drive new construction activity as well as upgrades to existing warehousing facilities over the medium term.

Grain Silos and Bulk Terminal Capacity in Egypt

-

By 2025, Egypt’s warehousing network consisted of between 80 and 90 grain silos across the country.

-

The mechanical handling systems installed at both port and inland terminals, such as conveyors and vertical elevators, generally support throughputs ranging from a few hundred tons to over a thousand tons per hour, depending on facility scale.

-

At Arish Port, the bulk terminal development completed in 2023 incorporates half a dozen cement silos, offering a combined storage capacity of around sixty thousand tonnes, with each unit able to hold roughly ten thousand tonnes.

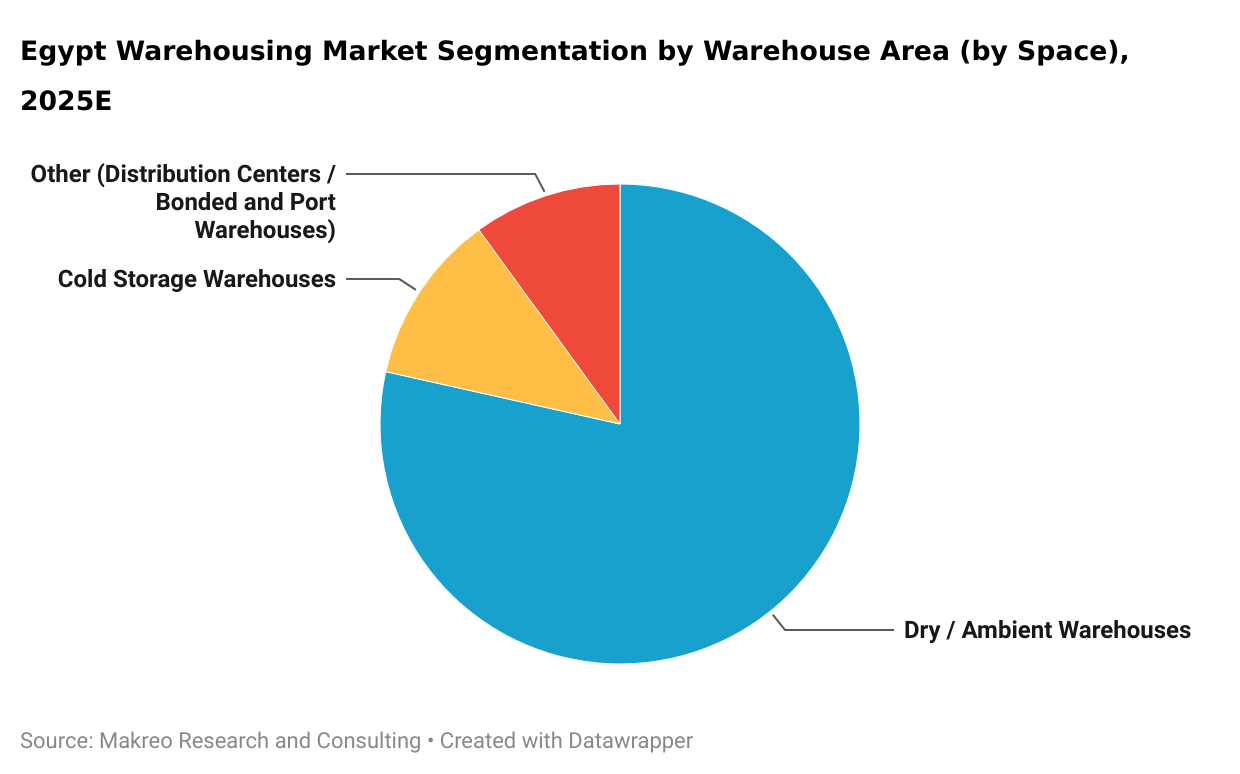

Warehouse Type Distribution in the Egypt Warehousing Market

-

Dry / Ambient Warehousing Dominates Supply: In 2025, dry or ambient warehouses accounted for close to nine out of every ten facilities in the Egypt warehousing market. This dominance is underpinned by sustained demand from large domestic users across FMCG, retail, textiles, and industrial manufacturing. Key demand drivers include Juhayna, B.TECH, Misr Spinning & Weaving, and ElSewedy Electric, all of which rely heavily on cost-efficient, non-temperature-controlled storage to support large-scale distribution and production activities.

-

Cold Storage Remains a Smaller but Expanding Segment: Cold storage facilities represented less than one-tenth of total warehousing capacity in 2025. Expansion in this segment is driven by increasing requirements from food processors, agribusinesses, and pharmaceutical distributors. Key users include Lactalis Egypt, Wadi Group, pharmaceutical distributors such as UPA, and fresh-produce exporters supported by Multi Fruit Egypt.

Macroeconomic and Sectoral Drivers Influencing Egypt’s Warehousing Demand

-

Egypt is targeting an increase in the industrial sector’s contribution to GDP from the mid-teens to approximately 20% by 2030, reflecting a sustained policy focus on manufacturing-led economic growth.

-

The ICT sector remained one of the top three contributors to national economic expansion in Q1 FY 2024/25 and continued its strong momentum with growth approaching the mid-teens percentage range in Q3 FY 2024/25.

-

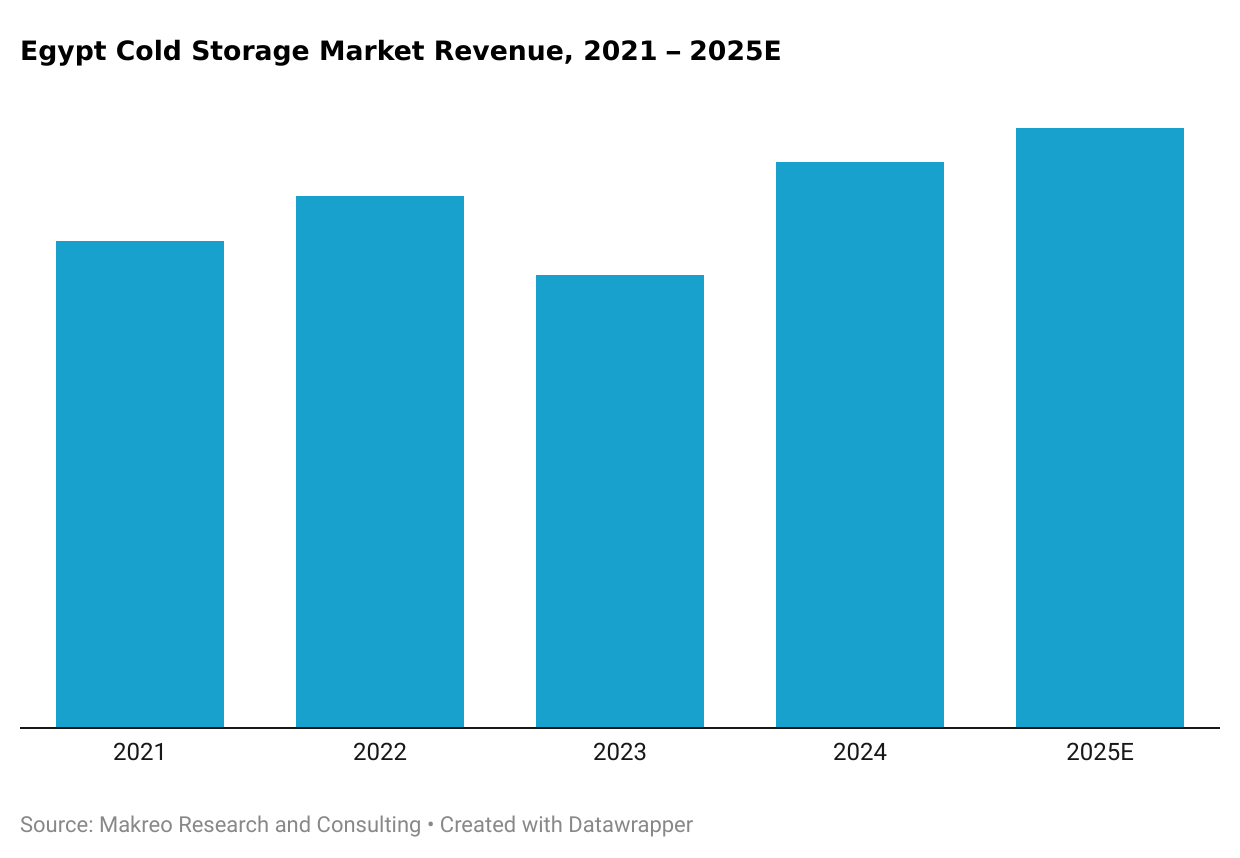

Food-processing exports exceeded USD 6 billion in 2024, representing over 20% year-on-year growth. This expansion is increasing pressure on refrigerated warehousing, temperature-controlled logistics, and export freight capacity, particularly across port-linked and cold chain infrastructure.

-

The construction sector is expected to grow at a single-digit annual rate during 2025–2030, sustaining demand for the movement and storage of cement, steel, glass, and other building materials. This trend supports continued requirements for near-site warehousing, port handling, and inland transport services.

-

Corn production for MY 2025/26 is projected to reach just over 7 million metric tonnes, reflecting a single-digit increase year-on-year. Growth is driven by an expansion in harvested area to nearly 1 million hectares, up by around 30,000 hectares from the previous season.

Egypt’s Strategic Push Toward Modern Logistics and Warehousing

Under Egypt Vision 2030, the government is positioning Public–Private Partnerships (PPPs) as a central mechanism to accelerate development across the logistics, warehousing, and cold chain market. Through the Ministry of Finance’s PPP Central Unit, Egypt is actively engaging private-sector investors to develop dry ports, logistics parks, cold chain hubs, and green transport infrastructure. These PPP structures typically grant private partners long-term concessions to design, finance, construct, and operate assets, enabling capital mobilization while advancing modernization of the national logistics backbone.

At the same time, Egypt is undertaking a comprehensive modernization of its logistics and industrial ecosystem, with significant investments directed toward smart ports, multimodal freight corridors, dry ports, and industrial zones. Digital transformation is becoming a core feature of this expansion, with technologies such as IoT-based tracking, port community systems, automated customs processes, and big-data analytics being integrated to improve connectivity, enhance transparency, and optimize supply-chain performance across the country.

-

2021 - 2025: Past and Present Scenario

-

2025: Base year of study

-

2025 - 2030: Outlook

Egypt Warehousing and Cold Chain Market Segmentation

-

Dry/Ambient Warehouses

-

Cold Storage Warehouses

-

Other (Distribution Centers / Bonded & Port Warehouses)

-

Large Warehouses

-

Medium Warehouses

-

Small Warehouses

Region Assessed

-

Greater Cairo (incl. 6th Oct)

-

Alexandria

-

Suez Canal / Port region

-

Other regions

-

Cold Storage

-

Cold Transport

-

Chilled (0–10°C)

-

Frozen (below −18°C)

-

Deep Frozen (below -25)

-

Food & Beverage (Meat, Dairy, Fruits & Vegetables)

-

Pharmaceuticals / Healthcare

-

Agriculture & Horticulture

-

Quick Service Restaurants (QSR)

-

Greater Cairo

-

Alexandria

-

Suez Canal / Port Cities

-

Upper Egypt / Delta

-

Competition

-

Warehousing Market Competitive Landscape

-

Cold Chain Market Competitive Landscape

-

-

Mergers, Acquisitions, and Investments

-

Funding Timeline

-

Company Profiles

Scope of the Study for Egypt Warehousing avnd Cold Chain Market

Makreo Research’s report, “Egypt Warehousing and Cold Chain Market Size and Forecast (2021–2030) - Analysis by Warehouse Type, Temperature Range (Chilled, Frozen, Deep-Frozen), Cold Storage Capacity, End-Use Industry and Geography”. The report examines how expanding industrial activity, rising consumer demand, and increasing domestic and international trade flows are reshaping storage requirements. It highlights Egypt’s growing role as a regional distribution hub, with rising demand for modern warehousing, efficient storage solutions, and reliable cold chain infrastructure across key sectors, including food and beverage, pharmaceuticals, and retail.

Egypt Warehousing Market Assessment and Infrastructure Analysis

-

Supply, distribution, and quality of warehousing infrastructure, including variations in facility standards and specifications.

-

Major logistics hubs, with a focus on Greater Cairo, Alexandria, and Suez Canal–linked cities, which anchor national distribution and trade flows.

-

Warehouse stock levels and capacity additions, assessing recent developments and upgrades across industrial and logistics parks.

-

Occupancy trends and the rise of Grade A industrial parks

Egypt Cold Chain Market Analysis

The report presents a focused assessment of Egypt’s cold chain sector, examining:

-

Cold storage capacity and temperature segmentation, including chilled, frozen, and deep-frozen facilities.

-

Availability and coverage of temperature-controlled transportation across domestic and export logistics networks.

-

Demand drivers across key end-use sectors, notably agribusiness, processed food, pharmaceuticals, and export-oriented supply chains.

Key Developments Enhancing Egypt’s Warehousing and Cold Chain Market

This section examines recent developments strengthening Egypt’s storage and distribution ecosystem, including:

-

Capacity expansions across warehousing and cold storage facilities.

-

Infrastructure upgrades improving operational efficiency and throughput.

-

Adoption of modern storage and handling technologies to enhance reliability and scalability.

-

Improvements within logistics corridors and industrial zones supporting faster distribution and trade-linked logistics.

Egypt Warehousing and Cold Chain Market Competitive Landscape

-

Key service providers operating across warehousing, cold storage, and temperature-controlled logistics.

-

Recent investments and capacity expansions shaping market scale and coverage.

-

Emerging operating models across logistics, storage, and cold chain segments, reflecting evolving customer and trade requirements.

Egypt Warehousing and Cold Chain Market Outlook

The report concludes with a forward-looking perspective driven by:

-

Ongoing regulatory reforms supporting sector modernization.

-

Rising industrial activity and consumer demand, particularly across food, pharmaceuticals, and retail.

-

Large-scale infrastructure investments across major logistics corridors and industrial zones, strengthening long-term growth prospects.

Companies Covered in the Egypt Warehousing and Cold Chain Market

-

Agility Logistics Egypt S.A.E.

-

Egyptian Global Logistics S.A.E

-

Transmar International Shipping Company

-

SulleX

-

Globelink Egypt

There are 11 players covered in this report. To know more, please reach out to sales@makreo.com

Table of Contents

- 1.Research Methodology

- 1.1.Objective of the Study

- 1.2.Market Definitions and Key Terminologies

- 1.3.Research Design and Procedure

- 1.4.Research Methodology

- 1.5.Data Collection Methods

- 2.Egypt Warehousing Market Past and Present Performance

- 2.1.Egypt Warehousing Market - An Overview

- 2.2.Egypt Warehousing Market Past and Present Performance

- 2.3.Egypt Warehousing Market – Demand and Supply Insights

- 3.Egypt Warehousing Market Segmentation

- 3.1.Egypt Warehousing Market Segmentation Overview

- 3.1.1.Egypt Warehousing Market Segmentation by Warehouse Type

- 3.1.2.Egypt Warehousing Market Segmentation by Warehouse Area

- 3.1.3.Egypt Warehousing Market Segmentation by Regions

- 3.1.Egypt Warehousing Market Segmentation Overview

- 4.Egypt Warehousing Rental Rates

- 4.1.African Countries Warehousing Rental Rates Comparison

- 4.2.Egypt Warehousing Rental Rates

- 4.3.Cairo Warehousing Rental Rates

- 4.4.Alexandria Warehousing Rental Rates

- 5.Cairo Warehouse Area and Rental Rates Analysis

- 5.1.Cairo Major Warehousing Nodes

- 5.2.Cairo Supply and Demand Analysis

- 6.Egypt Different Types of Warehouses by State/Territory

- 7.Egypt Warehouse Silos Analysis

- 8.Egypt Cold Chain Market Past and Present Performance

- 8.1.Egypt Cold Chain Market – An Overview

- 8.2.Egypt Cold Chain Market Past and Present Performance

- 9.Egypt Cold Chain Market Segmentation

- 9.1.Egypt Cold Chain Market Segmentation Overview

- 9.1.1.Egypt Cold Chain Market Segmentation by Function

- 9.1.2.Egypt Cold Chain Market Segmentation by Temperature Range

- 9.1.3.Egypt Cold Chain Market Segmentation by End-Use Industry

- 9.1.4.Egypt Cold Chain Market Segmentation by Geography

- 9.1.Egypt Cold Chain Market Segmentation Overview

- 10.Egypt Cold Chain Facilities and Capacities

- 10.1.Egypt Cold Storage Facilities by State/Territory

- 10.2.Egypt Key Players Cold Transport Capacities

- 11.Egypt Warehousing and Cold Chain Market Future Outlook

- 11.1.Egypt Warehousing Market Future Outlook

- 11.2.Egypt Cold Chain Market Future Outlook

- 12.Egypt Key Industry Analysis

- 12.1.Egypt Key Industry Market Overview

- 12.2.Egypt Food & Retail Industry Landscape

- 12.3.Egypt Pharmaceutical Manufacturing Capacity and Future Investment Outlook

- 12.4.Egypt Automotive Manufacturing Capacity and OEM Partnerships

- 12.5.Egypt E-commerce Landscape and Online Trends

- 13.Egypt Trade Performance

- 13.1.Egypt Trade Performance Overview

- 13.2.Egypt Export of Goods Trends

- 13.3.Egypt Import of Goods Trends

- 14.Egypt Warehousing Market Competitive Landscape

- 14.1.Egypt Top Players by Warehousing Space

- 14.2.Egypt Warehousing Market Area and Capacity

- 14.3.Egypt Warehousing Market Warehouse Footprint & Logistics Park Space

- 14.4.Egypt Warehousing Market Certifications and Compliances

- 15.Egypt Cold Chain Market Competitive Landscape

- 15.1.Egypt Cold Storage Key Players Capacity Comparison

- 15.2.Egypt Cold Storage Market Key Players by Temperature Ranges

- 15.3.Egypt Top Companies Fleet Size and Key Metrics Comparison

- 16.Mergers /Acquisitions/ Investments/ Disinvestments

- 16.1.Mergers /Acquisitions/ Investments/ Disinvestments

- 17.Funding Timeline

- 17.1.Funding Timeline

- 18.Egypt Warehousing Company Profiles

- 18.1.Player 1 – Business Overview

- 18.2.1.Business Highlights

- 18.2.2.Business Financials

- 18.2.Player 2 - Business Overview

- 18.2.1.Business Highlights

- 18.3.Player 3 - Business Overview

- 18.4.Player 4 - Business Overview

- 18.4.1.Timeline

- 18.4.2.Business Highlights

- 18.5.Player 5 - Business Overview

- 18.5.1.Business Highlights

- 18.5.2.Business Financials

- 18.6.Player 6 - Business Overview

- 18.7.Player 7 - Business Overview

- 18.8.Player 8 - Business Overview

- 18.8.1.Business Overview and Highlights

- 18.8.2.Service Scope, Market Share, and Facility Details

- 18.1.Player 1 – Business Overview

- 19.Egypt Cold Chain Logistics Company Profiles

- 19.1.Player 1 - Business Overview

- 19.2.Player 2 - Business Overview

- 19.3.Player 3 - Business Overview

- 20.Egypt Warehousing and Cold Chain Market Challenges

- 21.Egypt Warehousing and Cold Chain Market Opportunities

- Limitations of the Study

Related Reports — Automotive & Transportation