India Warehousing and Cold Chain Market Size and Forecast (2018-2030) - Focus on Growth Trends, Segmentation by Structure, Services, Ownership, and Key Cities

Overview

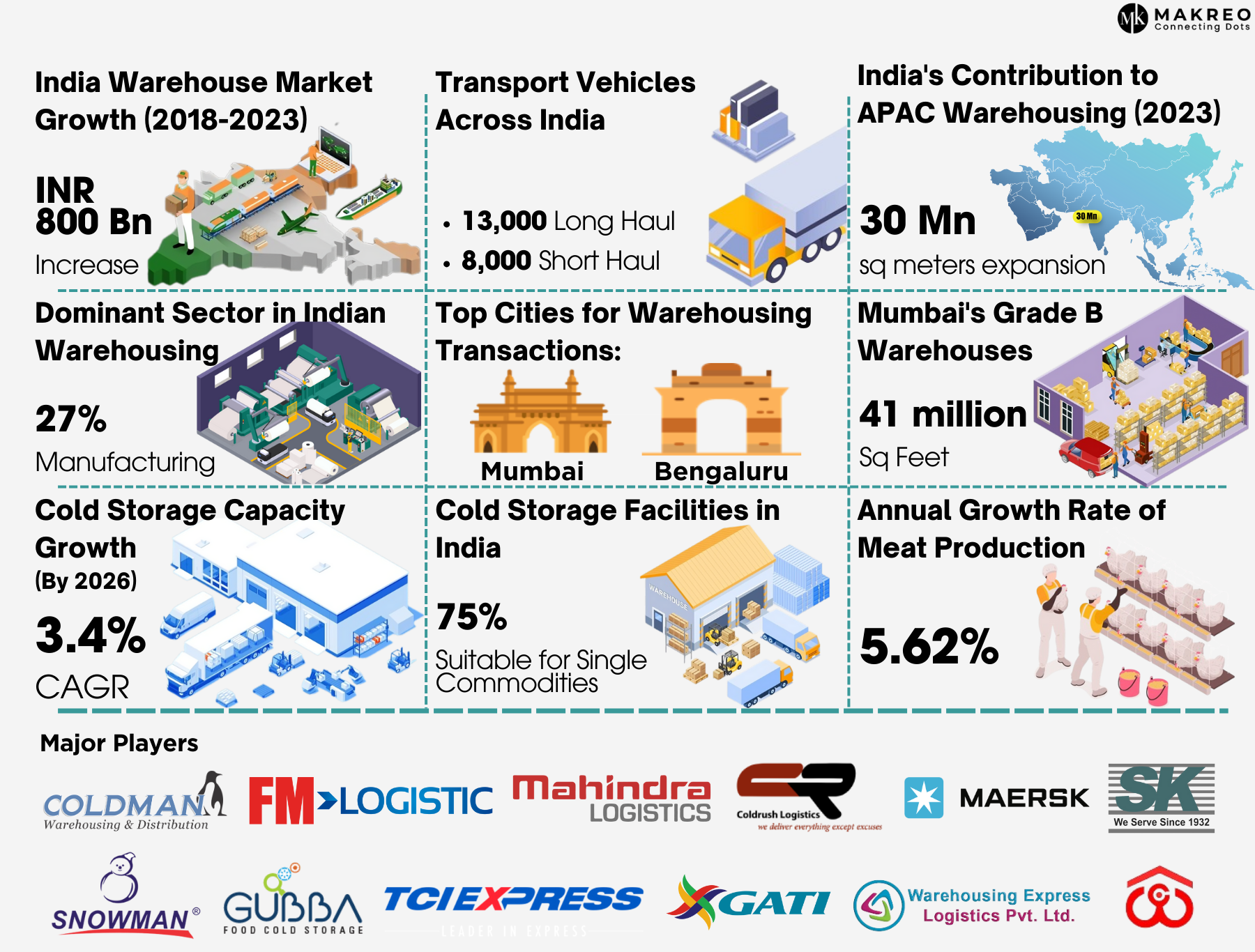

India Warehousing and Cold Chain Market Overview

The India warehousing and cold chain market has experienced remarkable growth and transformation over the past decade, largely driven by the implementation of the Goods and Services Tax (GST), which has facilitated the consolidation of warehousing operations and the development of larger, more centralized facilities. Indian warehouses now come in various forms, including traditional, automated, and temperature-controlled types, each tailored to meet the evolving demands of the market.

The warehousing industry in India encompasses a broad spectrum of services, including storage, transportation, inventory management, order fulfillment, and a range of value-added solutions. Parallel to this, the cold chain logistics sector is focused on the temperature-sensitive transportation and storage of goods, ensuring that products like pharmaceuticals, perishable food items, and other sensitive goods are maintained at optimal conditions throughout their journey.

These warehouses, which cater to diverse industries, are operated by a mix of logistics companies, manufacturers, retailers, and third-party logistics (3PL) providers. Their sizes vary significantly, with some designed to meet small-scale storage needs and others functioning as large-scale distribution centers that manage high volumes of goods. Key sectors benefiting from these facilities include e-commerce, retail, pharmaceuticals, food and beverages, and automotive industries.

Strategically located in industrial hubs such as Mumbai, Delhi-NCR, Bangalore, Pune, Chennai, and Kolkata, these cities play a pivotal role in the Indian warehousing landscape, with growing demand for advanced logistics and distribution services.

The Indian warehousing sector is comprised of both public and private warehouses. Public warehouses, typically managed by government entities like the Central Warehousing Corporation (CWC) and State Warehousing Corporations (SWCs), serve a wide array of industries, fulfilling diverse logistical needs across the country.

Performance of India’s Logistics and Warehousing Sector

India's logistics and warehousing sector is undergoing significant transformation, fueled by governmental support, robust infrastructure development, and technological advancements. The shift from conventional storage systems to modern, technology-integrated facilities is gaining substantial traction, with innovations in automation and warehouse management systems (WMS) boosting operational efficiency across the industry.

The demand for cold chain logistics remains strong, particularly from the pharmaceutical, food, and retail industries, positioning India as a leader in temperature-sensitive storage solutions. There has been a marked increase in investment in advanced warehousing, including Grade A facilities, driven by the need for enhanced supply chain optimization and the continued expansion of e-commerce.

Looking ahead, India’s warehousing and cold chain sectors will experience growth driven by the development of new logistics corridors, increased private sector involvement, and strategic mergers and acquisitions. Additionally, the industry's growing focus on sustainability, green warehousing, and AI-powered logistics solutions is set to reshape the landscape of India’s warehousing sector in the coming years.

Demand and Investment Trends in the India Warehousing Market

The warehousing, industrial, and logistics (WIL) sectors are expected to play a crucial role in supporting India's goal of achieving a USD 5 trillion economy by FY25.

As reported by FICCI India, the warehousing market has seen a significant influx of investments in recent years. India is projected to meet the demand for 223 million square feet of Grade-A warehousing space within the next three years. In 2019, India attracted USD 1,369 million in investments, although this decreased to USD 847 million in the following year. Western nations contributed significantly to India’s growth, with investments totaling USD 1,293 million, which further increased to USD 1,856 million in the subsequent year.

Demand for Grade A and Grade B Warehouses in India

Grade A warehouses typically command higher rental rates compared to Grade B and C warehouses, primarily due to their superior construction standards and modern facilities. However, when evaluating factors such as rental rates in India (INR per square foot per month), storage and cargo handling capacities, as well as pallet capacity in relation to volume, Grade A warehouses offer greater cost-efficiency, making them a more attractive option in comparison to Grade B and C warehouses.

In 2021, India’s warehousing market saw a year-on-year increase in the total stock of Grade A and Grade B warehouse space, particularly in metropolitan areas. This trend is now expanding to non-metropolitan cities, driven by the availability of lower rental rates, further enhancing the demand for these types of warehouses.

India's Grade A Warehousing Market Growth - Key Hubs Driving Demand in MMR, Pune, Chennai, and Bengaluru

India's Grade A warehousing sector is experiencing remarkable growth, fueled by increasing demand driven by the country’s evolving logistics and industrial landscapes. Cities like the Mumbai Metropolitan Region (MMR), Pune, and NCR have emerged as major hubs, collectively accounting for a significant portion of the country's warehousing demand. These regions are benefitting from rising investments, the establishment of new manufacturing units, and a boom in e-commerce activity. Pune, in particular, is seeing an overwhelming demand for Grade A warehousing, contributing to more than 48% of the demand in the MMR-Pune region.

As India positions itself as a global manufacturing hub, companies are shifting from China or expanding their operations in India, further fueling warehousing demand. The country’s competitive advantage of low wages, technology-driven manufacturing, and business-friendly policies are expected to propel the market towards 300 million sq ft of warehousing stock by the end of 2025.

The rapid rise in demand for high-quality warehousing has created an opportunity for developers and investors, especially in emerging cities like Chennai and Bengaluru. These regions have witnessed a sharp increase in warehousing infrastructure, further solidifying their roles as critical logistics and manufacturing centers. The rising demand is largely being driven by sectors like third-party logistics, manufacturing, and electronics, which continue to occupy a significant share of the market. With ongoing expansion, the Indian warehousing market offers promising prospects for growth and development.

Generalized Services and Cold Storage Growth

According to Makreo Research, generalized logistics services continue to hold a dominant share in the India logistics and warehousing market, while specialized services remain a smaller contributor. However, cold storage demand and supply gaps have significantly expanded in recent years, driven by increased consumer demand and sector investments, particularly in the India cold storage market. The growth trajectory of cold storage warehouses in India, particularly in regions like North India, West India, East India, and South India, suggests further investment in cold storage capacity and cold chain logistics. This trend is also propelled by the evolving retail sector, which demands better infrastructure, thus enhancing the leasing potential for cold storage warehouses and Grade A warehousing solutions.

Mergers and Acquisitions (M&A) and Funding Timeline

The logistics and warehousing sector in India has seen a surge in M&A activities and funding events in recent years. The period between 2018-2019 marked a significant rise in mergers and acquisitions, as companies sought expansion and consolidation opportunities. The COVID-19 pandemic in 2020 disrupted supply chains, prompting companies to focus on resilience through improved logistics infrastructure in India. From 2021-2022, investments poured into smart warehousing and smart logistics technology, while strategic acquisitions and partnerships bolstered market positioning. Looking ahead to 2023-2024, the timeline anticipates a continuation of robust funding and M&A activity, with an emphasis on growth in premium warehousing leasing and the expansion of cold chain market capabilities across key industrial hubs in India, including cities like Chennai, Pune, and Bengaluru.

This evolving landscape presents lucrative warehousing investment opportunities in India, particularly for third-party logistics providers looking to capitalize on growth trends in India warehousing demand and cold storage rental rates. The continued demand for Grade A warehousing space and cold storage rental rates indicates strong market prospects moving forward into 2025.

Scope of the India Warehousing and Cold Chain Market Report

The comprehensive scope of work involves analyzing and forecasting the India Warehousing and Cold Chain Market from 2018 to 2030, with a specific focus on the warehouse and cold chain market. The analysis encompasses various dimensions, including market structure (traditional, automated, temperature-controlled), services offered (storage, transportation, inventory management), ownership models (logistics companies, manufacturers, 3PL providers), warehouse size, industry verticals served (e-commerce, retail, pharmaceuticals), geographical presence (major cities and industrial hubs), technology integration (WMS, automation), supply chain efficiency, government initiatives, market trends, and the competitive landscape. This approach provides a detailed understanding of the market's dynamics and prospects across different facets of the warehousing and cold chain industry in India.

The report presents a comprehensive forecast for the Indian warehousing and cold chain market, extrapolating trends to offer insights into future growth prospects. This forward-looking analysis serves as a valuable resource for investors, policymakers, and industry participants, enabling them to make well-informed decisions. Anticipated growth in the warehousing and cold chain markets is expected to persist throughout the forecast period, propelled by the expansion of e-commerce, advancements in technology, and rising demand for temperature-sensitive storage. The adoption of technologies such as automation and data analytics in warehouse management is poised to enhance efficiency and reduce operational costs. Strategic investments in infrastructure, particularly in the development of modern warehouses, will play a pivotal role in meeting the escalating demand and establishing a resilient supply chain network.

- 2018 – 2023: Past and Present Scenario

- 2023 – Base Year

- 2024 – 2030: Future Outlook of the Industry

Segmentation by Structure

- Organized Sector

- Unorganized Sector

Segmentation by Warehousing and Cold Chain Services

- Generalized

- Specialized

Refrigerated/Cold Storage

Segmentation by Industry

Segmentation by Ownership

- Public Warehouses

- Private Warehouses

Segmentation by Size

- Grade A

- Grade B

Segmentation by Cities

-

What is the overall size and growth trajectory of the India Warehousing and Cold Chain Market from 2018 to 2030?

-

How is the market revenue distributed among Generalized, Specialized and Cold Chain warehouse structures?

-

What are the revenue trends based on industry-specific demands and which sectors are driving the demand for warehousing services?

-

How does infrastructure development, including technological advancements and facility improvements, influence the warehousing and cold chain market?

-

What is the breakdown of market revenue based on warehouse size categories and what are the preferences across different storage capacities?

-

How is the market revenue distributed among Generalized, Specialized, and Cold Chain services?

-

What is the revenue distribution based on ownership structures, including privately-owned and publicly-owned operated warehouses?

-

How does market revenue vary across major cities in India, and what are the regional growth patterns?

-

Who are the key players in the India Warehousing and Cold Chain Market, and what are their profiles, market share, and strategies?

-

What are the primary challenges faced by the warehousing and cold chain industry in India?

-

What opportunities exist for stakeholders in the evolving market landscape?

-

What are the potential threats to the warehousing and cold chain market, and how can they be mitigated?

Companies Covered

-

A.P. Moller-Maersk

-

FM Logistic India

-

SK Logistics

-

Warehousing Express Logistics Pvt. Ltd.

-

Coldman Logistics Pvt. Ltd.

-

Snowman Logistics Ltd.

-

Coldrush Logistics Pvt. Ltd.

-

Gati Ltd.

-

Gubba Green Cold Pvt. Ltd.

-

TCI Express Ltd.

-

Mahindra Logistics Ltd.

-

Central Warehousing Corporation

Looking for a Section from Report? Start your Partial Purchase Request

Table of Contents

- Report Synopsis

- Research Methodology

- Objective of the Study

- Research Process

- Data Collection Methods

- Analytical Framework

- 1.India Country Overview: EPTD Analysis

- 1.1.India EPTD Analysis

- 1.2.India Economic Overview

- 1.3.India Political Overview

- 1.4.India Technological Overview

- 1.5.India Demographic Overview

- 2.Asia Warehousing Market: Key Facts

- 2.1.Asia-Pacific Warehousing Market: An Overview

- 2.1.1.Warehousing Sector Potential in ASEAN Region

- 2.1.2.Asian Countries Occupied Cold Storage Space

- 2.1.3.Major Warehousing Countries in Asia-Pacific

- 2.1.Asia-Pacific Warehousing Market: An Overview

- 3.India Warehousing and Cold Chain Market: Past & Present Performance

- 3.1.India Warehouse & Cold Chain Infrastructure: An Overview

- 3.1.1.India Warehousing and Cold Chain Market – Past and Present Performance

- 3.1.2.Government Policies and Programs

- 3.1.3.India Warehousing Market Transactions

- 3.1.4.India Warehouse Absorption Rate

- 3.1.5.India Warehouse Annual Expansion

- 3.2.India Warehousing Market: Key Developments and Investments

- 3.3.India Warehouse Completion and Expected Period

- 3.4.Multi-Modal Logistics Parks in India (MMLPs)

- 3.5.Top 10 Warehouses and Logistics Operators in India

- 3.1.India Warehouse & Cold Chain Infrastructure: An Overview

- 4.India Warehousing Market Segmentation

- 4.1.India Warehousing Market: Industry Structure

- 4.2.India Warehousing Market Segmentation: By Structure (Organized and Unorganized)

- 4.3.India Warehousing Market: By Services (Generalized, Specialized, Refrigerated / Cold Storage)

- 4.4.India Warehousing Market Segmentation: By Industries

- 4.4.1.India Warehouse Transaction Share

- 4.5.India Warehouse Market Segmentation: By Ownership

- 4.5.1.India Warehouse Market: by Warehouse Size (Grade A & Grade B)

- 4.5.2.India Warehouse Market: by Grade A and Grade B Vacancy Rates

- 4.5.3.India Warehouse Market: by Grade A and Grade B Rental Rates

- 4.6.India Warehousing Market: By Cities

- 4.6.1.India Warehouse Rental Rates by Cities

- 4.6.2.India Warehousing Market: Transactions by Cities

- 4.6.3.India Warehouse Supply Distribution by Cities

- 4.6.4.India Warehouse Industry Classification

- 4.6.5.Key Warehouse Clusters in Major Indian Cities

- 5.India Cold Chain Market and Segmentation

- 5.1.India Cold Chain Market Infrastructure

- 5.2.India Cold Chain Market: An Overview

- 5.2.1.India Cold Chain Infrastructure Key Facts

- 5.2.2.India Cold Storage Infrastructure Demand vs. Supply

- 5.2.3.Cold Storage Total Capacity in India

- 5.3.India Cold Chain Market Revenue: Past and Present Performance

- 5.4.India Cold Chain Market Segmentation: By Structure (Organized and Unorganized)

- 5.5.India Cold Chain Market Segmentation: By Services (Cold Storage & Cold Transport)

- 5.6.India Cold Transport Market Segmentation: By Vehicle Size

- 5.7.India Cold Chain Market Segmentation: By Sectors

- 6.India Warehousing and Cold Chain Market Infrastructure

- 6.1.India Cold Chain Facilities Deployment and Requirements

- 6.2.India Cold Storage Market Infrastructure

- 6.3.India Warehousing and Cold Chain Projects

- 6.4.India Multi-Storey Warehouse Potential

- 7.India Warehousing Market: By Ownership

- 7.1.India Warehouse Market by Ownership: An Overview

- 7.1.1.India Number of Public Warehouses

- 7.1.2.India Number of Public Warehouses Capacity

- 7.1.India Warehouse Market by Ownership: An Overview

- 8.India Warehousing and Cold Chain Market: Challenges and Opportunities

- 8.1.India Warehousing and Cold Chain Market Challenges

- 8.2.Opportunity in India Warehousing Market

- 8.3.Opportunity in India Cold Storage Market

- 9.India Warehousing and Cold Chain Market: Competitive Landscape

- 9.1.Major Warehouse Occupiers in India

- 9.2.Leading Logistics and Warehouse Developers in India

- 10.India Warehousing and Cold Chain Market: Mergers, Acquisitions and Funding

- 10.1.Mergers and Acquisitions

- 10.2.Funding Timeline

- 11.India Warehousing and Cold Chain Market: Company Profiles

- 11.1.Company Profile: A.P. Moller-Maersk

- 11.2.Company Profile: FM Logistic India

- 11.3.Company Profile: SK Logistics

- 11.4.Company Profile: Warehousing Express Logistics Pvt. Ltd.

- 11.5.Company Profile: Coldman Logistics Pvt. Ltd.

- 11.6.Company Profile: Snowman Logistics Ltd.

- 11.7.Company Profile: Coldrush Logistics Pvt. Ltd.

- 11.8.Company Profile: Gati Ltd.

- 11.9.Company Profile: Gubba Green Cold Pvt. Ltd.

- 11.10.Company Profile: TCI Express Ltd.

- 11.11.Company Profile: Mahindra Logistics Ltd.

- 11.12.Company Profile: Central Warehousing Corporation

- 12.India Warehousing and Cold Chain Market: Future Outlook

- 12.1.India Warehousing and Cold Chain Market Future Outlook

- 12.1.1.India Cold Chain Market Future Outlook

- 12.2.India Cold Chain Market Future Outlook

- 12.3.India Manufacturing Market Forecast

- 12.4.Key Drivers for Growth in India Warehousing

- 12.5.India Agriculture Warehouse Market Forecast

- 12.6.India E-commerce Market Forecast

- 12.7.Indian Economy Forecast

- 12.1.India Warehousing and Cold Chain Market Future Outlook

- Limitations of the Study

Related Reports - Automotive & Transportation